Financial Toxicity and Cancer Treatment (PDQ®): Treatment - Health Professional Information [NCI]

Financial Toxicity Associated With Cancer Care—Background and Prevalence

Introduction

A number of studies demonstrate that individuals with cancer are at higher risk of experiencing financial difficulty than are individuals without cancer.[

Background

Cancer is one of the most costly medical conditions to treat in the United States.[

At the same time, commercial insurers in the United States are shifting more direct medical care costs to patients through higher premiums, deductibles, and coinsurance and copayment rates. The 2016 Commonwealth Fund Biennial Health Insurance Survey indicated that 33% of insured adults aged 19 to 64 years had medical bill problems or accrued medical debt.[

Oral cancer drug–based treatments are frequently covered under patient pharmacy benefits' specialty tier, requiring high coinsurance that patients pay out of pocket. High cost-sharing plans, including tiered outpatient prescription formularies (i.e., copays that escalate depending on whether the drug is generic or branded, and by price) may be particularly troublesome for patients with cancer who are prescribed expensive oral chemotherapeutics. The proportion of health care plans with multitiered (>3) prescription formularies, in which expensive oral specialty drugs are associated with the highest cost sharing, increased from 3% in 2004 to nearly 88% in 2017.[

Compared with individuals without a cancer history, cancer survivors have higher out-of-pocket costs, even many years after initial diagnosis,[

A number of other terms have been used to describe the financial impact of cancer, its treatment, and the lasting effects of treatment, including financial distress, financial stress, financial hardship, financial burden, economic burden, and economic hardship.[

Etiology and Risk Factors

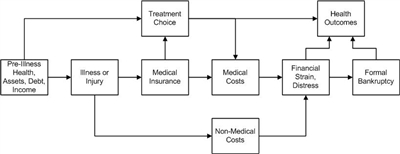

The interplay between cancer and financial distress is complex and related to a number of factors, as shown in

Figure 1. Conceptual framework relating severe illness, treatment choice, and health and financial outcomes. Credit: Scott Ramsey, MD, PhD.

Several factors in a household at the time a member of that household is diagnosed with cancer influence vulnerability to financial distress. The risk of severe financial distress and the period between illness and these outcomes are influenced by the following factors:

- Wage-earner status of the affected household member (primary, secondary, etc.).

- Pre-illness debt load.

- Assets.

- Illness-associated costs.

- The influence of the illness and its treatment on ability to work.

- The presence and terms of the health and disability insurance of the patient.

- Incomes of others in the household.

At the time of cancer diagnosis, several factors that determine the long-range risk of financial hardship include the following:

- The general health and noncancer comorbidities of the patient.

- Assets.

- Existing debt.

- Household income.

- A household with income from other sources, such as a spouse or family member who works outside the home.

Components of these measures include material conditions that arise from increased out-of-pocket expenses, lower income from the inability to work, and psychological response to increased household expenses and reduced income.[

The material conditions of patients and their families that may be adversely affected by a cancer diagnosis and treatment are typically measured as follows:[

- Out-of-pocket medical costs.

- Out-of-pocket costs as a percentage of income.

- Reduction in income and assets.

- Medical debt.

- Trouble paying medical bills and for necessities (e.g., housing, food).

- Bankruptcy.

In addition, a patient's psychological response to increased financial burden associated with a cancer diagnosis and treatment is typically measured as financial stress, distress, or worry.[

Prevalence

A number of studies have measured components of at least one aspect of financial hardship,[

The following sections describe the prevalence of specific measures of financial hardship, including out-of-pocket costs, productivity loss, asset depletion and medical debt, bankruptcy, and financial distress and worry.

Prevalence of high out-of-pocket costs

Out-of-pocket costs, one of the most common measures of financial hardship, are the amounts that patients pay directly for their medical care. They include insurance copayments, coinsurance, and deductibles for prescription and nonprescription medications, hospitalizations, outpatient services, and other types of medical care.[

In a study of long-term breast cancer survivors, 18% paid between $2,001 and $5,000 in out-of-pocket expenses, and 17% paid more than $5,000.[

In a study conducted using the nationally representative Medical Expenditure Panel Survey (MEPS), 4.3% of cancer survivors aged 18 to 64 years reported a high out-of-pocket burden, compared with 3.4% of those without a cancer history.[

Prevalence of productivity loss

Productivity loss is typically measured as the inability to work or pursue usual activities, days lost from work or disability days, reduction in work hours, and days spent in bed. Productivity loss may be quantified directly from employment data [

Prevalence of asset depletion and medical debt

Several studies have reported the prevalence of asset depletion and medical debt for cancer survivors, although this information is rarely reported in relation to individuals without a cancer history or before and after a cancer diagnosis. Further, most estimates are based on self-report, and little validation work has been conducted.

Studies of cancer survivors suggest that between 33% and 80% of the survivors have used savings to finance medical expenses,[

Incidence and prevalence of bankruptcy

One of the few studies to measure the incidence of financial hardship reported that 1.7% of cancer survivors filed for bankruptcy in the 5 years after diagnosis.[

Prevalence of financial stress, distress, or worry

Several studies have found a prevalence of financial stress and worry about paying medical bills for cancer ranging from 22.5% in a nationally representative sample [

Prevalence of financial hardship as a composite measure

Several studies combine multiple components of financial hardship using summary measures, scores, or measures, including the Comprehensive Score for Financial Toxicity (COST) measure and the Personal Financial Wellness (PFW) Scale (formerly known as the InCharge Financial Distress/Financial Well-Being [IFDFW] Scale), but the results are rarely presented in relation to the general population and can be difficult to interpret.

In a study of patients with multiple myeloma undergoing treatment at a single academic cancer center, cancer survivors had a mean COST score of 23 (range, 0–44, with lower values equivalent to higher burden).[

References:

- Ekwueme DU, Yabroff KR, Guy GP, et al.: Medical costs and productivity losses of cancer survivors--United States, 2008-2011. MMWR Morb Mortal Wkly Rep 63 (23): 505-10, 2014.

- Guy GP, Ekwueme DU, Yabroff KR, et al.: Economic burden of cancer survivorship among adults in the United States. J Clin Oncol 31 (30): 3749-57, 2013.

- Guy GP, Yabroff KR, Ekwueme DU, et al.: Estimating the health and economic burden of cancer among those diagnosed as adolescents and young adults. Health Aff (Millwood) 33 (6): 1024-31, 2014.

- Guy GP, Yabroff KR, Ekwueme DU, et al.: Healthcare Expenditure Burden Among Non-elderly Cancer Survivors, 2008-2012. Am J Prev Med 49 (6 Suppl 5): S489-97, 2015.

- Bernard DS, Farr SL, Fang Z: National estimates of out-of-pocket health care expenditure burdens among nonelderly adults with cancer: 2001 to 2008. J Clin Oncol 29 (20): 2821-6, 2011.

- Davidoff AJ, Erten M, Shaffer T, et al.: Out-of-pocket health care expenditure burden for Medicare beneficiaries with cancer. Cancer 119 (6): 1257-65, 2013.

- Langa KM, Fendrick AM, Chernew ME, et al.: Out-of-pocket health-care expenditures among older Americans with cancer. Value Health 7 (2): 186-94, 2004 Mar-Apr.

- Soni A: Trends in the Five Most Costly Conditions among the U.S. Civilian Institutionalized Population, 2002 and 2012. Statistical Brief 470. Rockville, Md: Agency for Healthcare Research and Quality, 2015.

Available online . Last accessed May 28, 2024. - Bradley CJ, Yabroff KR, Warren JL, et al.: Trends in the Treatment of Metastatic Colon and Rectal Cancer in Elderly Patients. Med Care 54 (5): 490-7, 2016.

- Shih YC, Smieliauskas F, Geynisman DM, et al.: Trends in the Cost and Use of Targeted Cancer Therapies for the Privately Insured Nonelderly: 2001 to 2011. J Clin Oncol 33 (19): 2190-6, 2015.

- Conti RM, Fein AJ, Bhatta SS: National trends in spending on and use of oral oncologics, first quarter 2006 through third quarter 2011. Health Aff (Millwood) 33 (10): 1721-7, 2014.

- Gordon N, Stemmer SM, Greenberg D, et al.: Trajectories of Injectable Cancer Drug Costs After Launch in the United States. J Clin Oncol 36 (4): 319-325, 2018.

- Shih YT, Xu Y, Liu L, et al.: Rising Prices of Targeted Oral Anticancer Medications and Associated Financial Burden on Medicare Beneficiaries. J Clin Oncol 35 (22): 2482-2489, 2017.

- 2016 Biennial Health Insurance Survey. New York, NY: The Commonwealth Fund, 2017.

Available online. Last accessed May 28, 2024. - 2017 Employer Health Benefits Survey. San Francisco, Calif: Henry J. Kaiser Family Foundation, 2017.

Available online. Last accessed May 28, 2024. - Tucker-Seeley RD, Yabroff KR: Minimizing the "financial toxicity" associated with cancer care: advancing the research agenda. J Natl Cancer Inst 108 (5): , 2016.

- de Souza JA, Yap B, Ratain MJ, et al.: User beware: we need more science and less art when measuring financial toxicity in oncology. J Clin Oncol 33 (12): 1414-5, 2015.

- Smith R, Clarke L, Berry K, et al.: A comparison of methods for linking health insurance claims with clinical records from a large cancer registry. [Abstract] Med Decis Making 21 (6): 530, 2001.

- Fay S, Hurst E, White MJ: The household bankruptcy decision. Am Econ Rev 92 (3): 706-18, 2002.

- Banegas MP, Guy GP, de Moor JS, et al.: For Working-Age Cancer Survivors, Medical Debt And Bankruptcy Create Financial Hardships. Health Aff (Millwood) 35 (1): 54-61, 2016.

- Yabroff KR, Dowling EC, Guy GP, et al.: Financial Hardship Associated With Cancer in the United States: Findings From a Population-Based Sample of Adult Cancer Survivors. J Clin Oncol 34 (3): 259-67, 2016.

- Chang S, Long SR, Kutikova L, et al.: Estimating the cost of cancer: results on the basis of claims data analyses for cancer patients diagnosed with seven types of cancer during 1999 to 2000. J Clin Oncol 22 (17): 3524-30, 2004.

- Ell K, Xie B, Wells A, et al.: Economic stress among low-income women with cancer: effects on quality of life. Cancer 112 (3): 616-25, 2008.

- Jagsi R, Pottow JA, Griffith KA, et al.: Long-term financial burden of breast cancer: experiences of a diverse cohort of survivors identified through population-based registries. J Clin Oncol 32 (12): 1269-76, 2014.

- Meisenberg BR, Varner A, Ellis E, et al.: Patient Attitudes Regarding the Cost of Illness in Cancer Care. Oncologist 20 (10): 1199-204, 2015.

- Meneses K, Azuero A, Hassey L, et al.: Does economic burden influence quality of life in breast cancer survivors? Gynecol Oncol 124 (3): 437-43, 2012.

- Ramsey S, Blough D, Kirchhoff A, et al.: Washington State cancer patients found to be at greater risk for bankruptcy than people without a cancer diagnosis. Health Aff (Millwood) 32 (6): 1143-52, 2013.

- Shankaran V, Jolly S, Blough D, et al.: Risk factors for financial hardship in patients receiving adjuvant chemotherapy for colon cancer: a population-based exploratory analysis. J Clin Oncol 30 (14): 1608-14, 2012.

- Regenbogen SE, Veenstra CM, Hawley ST, et al.: The personal financial burden of complications after colorectal cancer surgery. Cancer 120 (19): 3074-81, 2014.

- Veenstra CM, Regenbogen SE, Hawley ST, et al.: A composite measure of personal financial burden among patients with stage III colorectal cancer. Med Care 52 (11): 957-62, 2014.

- Wan Y, Gao X, Mehta S, et al.: Indirect costs associated with metastatic breast cancer. J Med Econ 16 (10): 1169-78, 2013.

- Zafar SY, Peppercorn JM, Schrag D, et al.: The financial toxicity of cancer treatment: a pilot study assessing out-of-pocket expenses and the insured cancer patient's experience. Oncologist 18 (4): 381-90, 2013.

- Zajacova A, Dowd JB, Schoeni RF, et al.: Employment and income losses among cancer survivors: Estimates from a national longitudinal survey of American families. Cancer 121 (24): 4425-32, 2015.

- Finkelstein EA, Tangka FK, Trogdon JG, et al.: The personal financial burden of cancer for the working-aged population. Am J Manag Care 15 (11): 801-6, 2009.

- Jagsi R, Ward KC, Abrahamse PH, et al.: Unmet need for clinician engagement regarding financial toxicity after diagnosis of breast cancer. Cancer 124 (18): 3668-3676, 2018.

- Meisenberg BR: The financial burden of cancer patients: time to stop averting our eyes. Support Care Cancer 23 (5): 1201-3, 2015.

- Huntington SF, Weiss BM, Vogl DT, et al.: Financial toxicity in insured patients with multiple myeloma: a cross-sectional pilot study. Lancet Haematol 2 (10): e408-16, 2015.

This information does not replace the advice of a doctor. Ignite Healthwise, LLC, disclaims any warranty or liability for your use of this information. Your use of this information means that you agree to the

Healthwise, Healthwise for every health decision, and the Healthwise logo are trademarks of Ignite Healthwise, LLC.

Page Footer

I want to...

Audiences

Secure Member Sites

The Cigna Group Information

Disclaimer

Individual and family medical and dental insurance plans are insured by Cigna Health and Life Insurance Company (CHLIC), Cigna HealthCare of Arizona, Inc., Cigna HealthCare of Illinois, Inc., Cigna HealthCare of Georgia, Inc., Cigna HealthCare of North Carolina, Inc., Cigna HealthCare of South Carolina, Inc., and Cigna HealthCare of Texas, Inc. Group health insurance and health benefit plans are insured or administered by CHLIC, Connecticut General Life Insurance Company (CGLIC), or their affiliates (see

All insurance policies and group benefit plans contain exclusions and limitations. For availability, costs and complete details of coverage, contact a licensed agent or Cigna sales representative. This website is not intended for residents of New Mexico.